Made4net has been recognized in the 2026 Gartner® Magic Quadrant™ for Warehouse Management Systems (WMS) for the 11th consecutive year — a milestone that we feel reflects sustained momentum in a market being reshaped by cost pressure, automation, and the early stages of AI adoption.

According to the report, the WMS market continues to evolve amid shifting economic and operational pressures, noting that “Despite being a very mature market, recent macro factors and disruptions have spurred innovation. However, while economic and business conditions are challenging for some vendors and regions with regard to new customer acquisition, the overall market reached almost $3.5 billion in 2025. WMS offerings continue to differ in areas such as usability, adaptability, decision support, scalability in both up and down markets, use of emerging technologies and life cycle costs.”

So what does the 2026 report tell us about where the WMS market is headed and what buyers should prioritize? Here are Made4net’s key takeaways.

Core Functionality Is Now Table Stakes. Differentiation Has Shifted.

One of the most important findings in this year’s report is something many buyers still overlook: at the core WMS level, most vendors in the Gartner Magic Quadrant can meet your requirements. Functionality still matters, but it is no longer the primary differentiator among qualified solutions.

Gartner identifies near-functional parity across providers for basic capabilities, noting that “although functionality remains the primary user evaluation criterion, there’s near-functional parity for basic core WMS capabilities across WMS providers.” What now shapes vendor positioning is a broader set of factors: time to value, total cost of ownership, architecture flexibility, cloud strategy, implementation track record, quality of service and support, and long-term product viability.

All 18 vendors included in this year’s Magic Quadrant cleared a demanding qualification bar. The real question for buyers has shifted from whether a system can do the job to how it stands out from an innovation standpoint, and how efficiently it can be deployed, adapted, and operated over time.

Takeaway for buyers: Map the full set of Gartner vendor evaluation criteria against your own organizational priorities. All 18 vendors meet the baseline. In our view, the differentiators are in execution, cost, and fit over time.

Know Your Complexity Level Before You Start Shortlisting

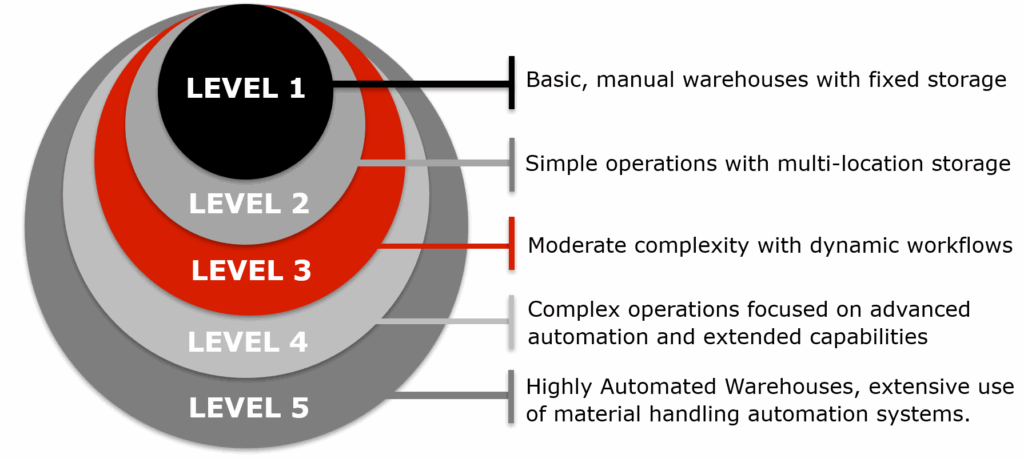

Our take on the most actionable theme in this year’s report is that warehouse operations exist across a wide spectrum of complexity, and buying the wrong level of solution is one of the most common and costly mistakes organizations make.

Gartner uses a five-level model to stratify warehouse complexity, from Level 1 (most basic) to Level 5 (most complex and automated). The report is direct: “globally, the preponderance of warehouse operations are Level 3 or below in Gartner’s warehouse complexity model. Warehouses at Level 3 and below do not require, nor would they normally use, the most advanced functionality.”

At the same time, Gartner acknowledges “a very clear market for high-end WMS solutions where feature/function and performance are critical and cost is not the highest priority.” Alongside that sits “another market where other factors dominate, such as ease of use, reliability, service and support, ‘good enough’ features and lower cost of ownership. This is a very large WMS market for what Gartner’s stratification model would call Level 2 and Level 3 warehouse environments.”

These are genuinely different markets with different criteria for success. Overbuying creates real problems: higher costs, longer deployments, and functionality that never gets used. Underbuying limits growth and can force a painful re-implementation as operations evolve.

Amit Levy, EVP of Sales and Strategy at Made4net, explains that, “Buyers are increasingly using Gartner’s Level 1 to 5 operational complexity model to assess WMS fit. They’re asking whether a solution meets current needs and can scale with future growth and automation goals. At the end of the day, the best WMS isn’t the one with the most features. It’s the one that aligns best with your strategy.”

Takeaway for buyers: Use the Gartner stratification model to assess your current and realistic future complexity level before evaluating vendors. Your complexity profile should drive your shortlist, not the other way around.

For Large Organizations, One WMS Rarely Fits the Whole Network

For companies operating multiple facilities, the challenge grows considerably. Gartner puts it plainly: “To support diverse operations, organizations have warehouse operations that span from very simple Level 1 warehouses to highly complex and automated Level 5 warehouses, and everything in between. While functional depth and breadth are important for the complex operations, simplicity and ease of use are much more compelling needs for Level 1 and Level 2 operations.”

A retailer or 3PL might run everything from a small regional DC to a highly automated fulfillment center within the same network, and the functional priorities at each end of that spectrum are genuinely different. A solution optimized only for Level 5 complexity imposes unnecessary cost and overhead on the rest of the network. A solution built for Level 2 and 3 will hit a ceiling as more demanding sites evolve.

In Made4net’s view, the answer is a configurable and adaptable solution that performs credibly across the full complexity spectrum without forcing either oversimplification or over-engineering. Made4net is recognized for scalable and adaptable solutions that consistently score well across many different warehouse complexities – from simple cross dock operations to fully automated warehouses with cutting edge MHE.

As Duff Davidson, CEO of Made4net, frames it, “Our recognition in the 2026 Gartner Magic Quadrant reflects our focus on delivering a flexible WMS that deploys quickly, scales pragmatically, and provides a strong foundation for AI-enabled decision support without adding unnecessary complexity or cost.”

Takeaway for buyers: If your network spans multiple complexity levels, evaluate vendors across all relevant use cases. Score them on the full range, not just the most demanding site.

Labor Challenges Continue to Drive Technology Decisions

Labor is not a new issue in warehousing, but it remains one of the most powerful forces driving WMS investment in 2026. Gartner notes that “customers now focus more attention on the value-adding capabilities that surround core WMS capabilities, due to the compelling need to address labor shortages and rising costs. Examples include workforce management, task interleaving, slotting, yard management, dock scheduling and performance management. These have now become common requirements in all but the most basic WMS deals.”

Beyond capability requirements, persistent labor shortages are accelerating automation investment at every level of complexity. Gartner observes that “labor shortages are motivating companies to consider various forms of automation — from intralogistics smart robotics increasingly found across various strata of operations, to complex conventional material handling automation systems that are often found in Level 5 warehouse operations.”

Duff Davidson puts it plainly, “Warehouse operators are being asked to do more with less while preparing for a more automated, AI-driven future.”

The implication for WMS selection is significant. The execution platform a company deploys today needs to function as a credible foundation for the automated environment it is building toward. Vendors that support both manual and automated operations on a unified platform are better positioned to serve this evolution without requiring costly re-implementation.

Takeaway for buyers: Evaluate vendors on their automation roadmap and architecture, not just their current integration list. Labor pressures will only intensify. Your WMS needs to be ready from a technology and architecture perspective, for current automation enablers, and also for what the future may bring.

Pricing Is Under More Scrutiny Than Ever, and Getting More Complicated

If there is a single theme running through every section of this year’s report, we feel it is that buyers are paying far closer attention to total cost of ownership. And the pricing environment is not getting simpler.

Cloud has become the dominant direction, with more than 85% of new customers preferring cloud deployment when the economics are sound. But Gartner notes that “for larger and more complex environments, WMS cloud pricing is confusing to buyers since a de facto standard pricing model remains elusive, and long-term (10- to 15-year) costs seem unreasonably high to many buyers.” On top of that, the shift away from named-user pricing toward models based on order lines, license plate numbers, and other metrics makes vendor comparisons increasingly difficult.

AI is now adding another layer of complexity. Gartner observes that “the necessity of supporting consumption-based pricing for use of AI will disrupt subscription-based pricing just at the point when it had begun to stabilize.” The vendors best positioned to compete in this environment are those offering genuine flexibility in commercial terms, across deployment models, pricing structure, and the ability to opt in or out of advanced capabilities based on operational need.

Takeaway for buyers: Model total cost of ownership carefully, not just year-one licensing. Flexibility in commercial terms is increasingly a real competitive differentiator, not a negotiating concession.

Cloud Has Won. Now the Real Questions Begin.

The deployment debate has largely been settled. More than 85% of new WMS deals are cloud, and migration from on-premises legacy systems continues steadily. But the cloud story in WMS is more nuanced than the headline number suggests.

For lower-complexity environments, subscription-based cloud pricing has meaningfully reduced short-term costs and fueled market interest. For enterprise-scale deployments, the combination of confusing pricing models, long-term cost uncertainty, and the dedicated versus multitenant architecture debate makes cloud decisions considerably more involved.

Takeaway for buyers: Cloud is the right direction for most organizations, but treat it as a multi-dimensional decision. Evaluate architecture, security track record, hyperscaler flexibility, and long-term pricing implications as independent criteria.

AI Is Advancing, but Practical Impact Is Still Developing

AI is one of the most prominent themes in the 2026 report, with virtually every vendor building out capabilities across generative AI, agentic AI, and vision AI. Gartner describes the current state: “many vendors have adopted limited forms of basic AI and machine learning to add more sophisticated intelligence to their applications. More recently, some vendors have begun restructuring to enable agentic AI, with many now deploying GenAI to support data retrieval and ease of use.”

The next wave, encompassing decision support, optimization, and autonomous execution, is on nearly every vendor’s roadmap. Progress varies significantly. Organizations evaluating AI capabilities should focus less on which vendors claim the most impressive roadmap and more on which have embedded AI into execution in ways that are practical, priced transparently, and architecturally integrated rather than bolted on.

Made4net’s approach is deliberate. As Amit Levy describes, “As warehouses layer in automation and continue the journey of adopting AI, execution systems need to be unified, extensible, and operationally practical. Organizations are looking for robust capabilities alongside innovation, enabling them to use natural language interaction and intelligent automation at their own pace.”

Made4net’s 2026 AI foundation layer, including natural language-driven tools and planned configuration and execution agents, is designed to support this progression without requiring customers to move faster than their operations are ready for.

Takeaway for buyers: Ask vendors to share examples of how AI is being applied in their solutions today, alongside their future roadmap. Understand how AI capabilities will be priced. Assess whether the vendor’s architecture makes AI a native part of execution or a separate subscription sitting on top.

The Bottom Line: Fit Matters More Than Features

Our take is the 2026 Gartner Magic Quadrant reinforces a shift that has been building for years. Core functionality is no longer the differentiator. Complexity varies widely across operations and networks. Cost and time to value are under greater scrutiny. Flexibility and adaptability matter as much as feature depth.

The best WMS is not the most powerful one. It is the one that best fits your operation, today and as it evolves.

We believe Made4net’s eleven consecutive years of recognition in the Gartner Magic Quadrant reflects exactly this: a solution built to deliver pragmatic value across a wide range of environments, deploy efficiently, scale with operational growth, and provide a credible path to AI-enabled execution without adding unnecessary complexity or cost.

Want to explore the full 2026 Gartner Magic Quadrant for Warehouse Management Systems?

Download your complimentary copy here!

Disclaimer:

Gartner, Magic Quadrant for Warehouse Management Systems, By Simon Tunstall et. al, 29 April 2026

GARTNER is a trademark of Gartner, Inc. and/or its affiliates. Magic Quadrant is a registered trademark of Gartner, Inc. and/or its affiliates and is used herein with permission. All rights reserved.

Gartner does not endorse any company, vendor, product or service depicted in its publications, and does not advise technology users to select only those vendors with the highest ratings or other designation. Gartner publications consist of the opinions of Gartner’s business and technology insights organization and should not be construed as statements of fact. Gartner disclaims all warranties, expressed or implied, with respect to this publication, including any warranties of merchantability or fitness for a particular purpose.